| Better digital services |

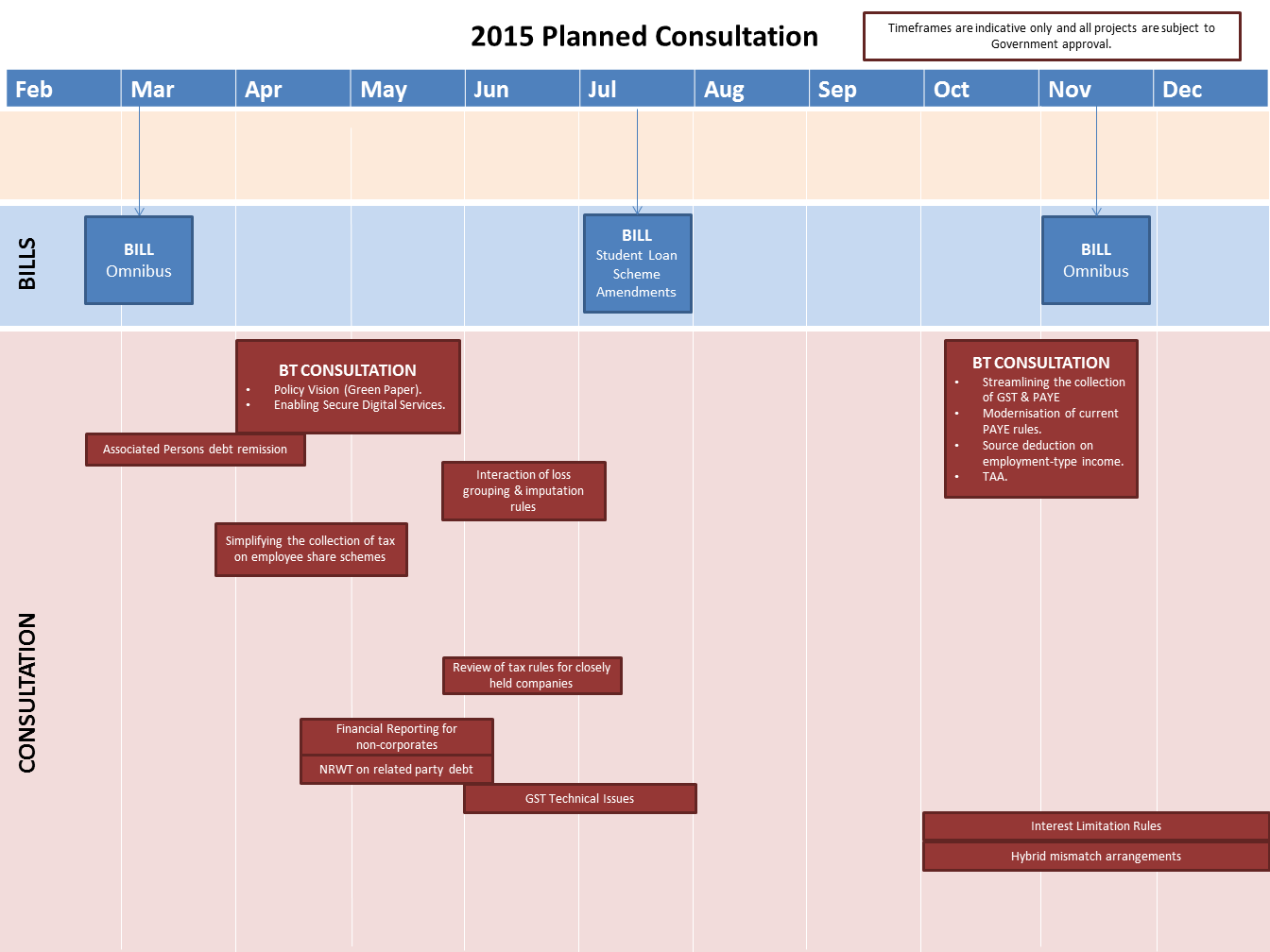

Work to ensure that the policy and legislative framework facilitates the implementation and delivery of secure digital services. |

| Review of the Tax Administration Act 1994 |

Development of a tax administration framework that fits the direction of BT. |

| Streamlining the collection of GST and PAYE |

Work to understand current payroll and GST processes, and develop new policy options consistent with longer-term BT thinking. |

| Modernisation of the current PAYE rules |

Consideration of the PAYE rules to see if they reflect modern employment practices and law. |

| Source deduction on employment-type income |

Investigate extending withholding taxes to cover employment-like income that falls outside the current rules. |

| Individual taxation |

Improving the tax system for individuals, including comprehensive pre-population of income information, collection of information, more efficient debt collection processes and considering the degree of interaction with the tax system. |

| Streamlining the collection of capital income withholding taxes |

Streamlining the collection of other withholding regimes information such as resident withholding tax and dividends. |

| Business taxation |

Improving the tax system for business, including the calculation of provisional tax, collection of information and reviewing the penalties and interest rules. |

| Encouraging better compliance with tax obligations |

Review the interest, penalty and debt rules.

Consider options to better encourage the filing of returns and the payment of tax.

Consider the information to be provided by large corporates to assist with risk analytics.

These matters will be considered as part of, and in conjunction with, the appropriate BT project.

|

| Better public services |

| Social-sector information-sharing agreement between Ministry of Social Development and the Accident Compensation Corporation and Inland Revenue |

Information-sharing with Ministry of Social Development and the Accident Compensation Corporation to assist in the determination of individual entitlements to benefits and services. |

| Sharing information about non-individuals |

Information-sharing about non-individuals to enable businesses to share information for compliance reasons. |

| Information-sharing – Targeting serious crime: Phase 2 |

Information-sharing with New Zealand Police for the prevention, detection, investigation or provision of evidence of a serious crime. |

| INTERNATIONAL TAX AND BASE EROSION AND PROFIT SHIFTING (BEPS) |

| Negotiation of double tax agreements |

Negotiation of new double tax agreements with Samoa, Luxembourg, Portugal and Slovak Republic. Negotiations to renew existing agreements with Norway, China, Korea and Australia. |

| Mutual recognition of imputation credits |

Working to progress mutual recognition of trans-Tasman imputation credits which would see both New Zealand and Australia recognising company tax paid in the other jurisdiction for imputation purposes. |

| Hybrid instruments and entities |

Consideration of hybrid instruments and entities in light of the OECD’s recommendations (part of the BEPS Action Plan). |

| Non-resident withholding tax on related-party debt |

Address problems with the application of non-resident withholding tax on interest on related-party debt. |

| Interest limitation rules |

Consideration of New Zealand’s interest limitation rules in light of the OECD’s recommendations (part of the BEPS Action Plan). |

| Automatic exchange of information |

Domestic implementation of a new global standard on the automatic exchange of financial bank account information with treaty partners. |

| Tax Information Exchange Agreements and Multilateral Convention on Mutual Administrative Assistance in Tax Matters |

On-going work to bring the Multilateral Convention on Mutual Administrative Assistance in Tax Matters into force for New Zealand. |

| Tax treaties and avoidance |

Work to clarify the relationship between the general anti-avoidance rules and double tax agreements. |

| Companies becoming treaty non-resident |

Work to address possible tax avoidance areas around the rules relating to companies becoming treaty non-resident. |

| GST on imports of services, intangibles and low-value goods |

Contributing to the OECD’s work on this issue and, in particular, purchases from offshore of services and intangibles such as digital downloads and low-value goods. Considering what this work means for New Zealand. |

| ENHANCEMENTS TO TAX AND SOCIAL POLICY WITHIN BROAD-BASE, LOW-RATE (BBLR) TAX SETTINGS |

| Tax policy |

| Review of tax rules for closely held companies and look-through companies |

Providing an improved framework and simplifying the legislation for closely held companies. |

| Review of the tax framework for employee share schemes |

Reviewing the policy framework for the taxation of employee share schemes. |

| Collection of tax at source on employee share scheme benefits |

Changes to allow tax liabilities on employee share scheme benefits to be satisfied through PAYE or FBT rather than requiring the employee to file a tax return. |

| Interaction of loss grouping and imputation rules |

Considering how to preserve the benefit of loss offsetting for shareholders of non-wholly owned groups. |

| Tax simplification for small to medium enterprises (SMEs) |

On-going monitoring and research to ensure this topic is represented in items on the work programme. |

| Financial reporting for non-corporates |

Developing minimum financial reporting requirements for businesses and certain other taxpayers. |

| Related-parties debt remission |

Analysis of the outcome of current law on related-parties debt remission. An officials’ issues paper was released for consultation in February 2015. |

| Local/regional promotion bodies’ exemption – application to trusts |

Review of the possible inclusion of trusts in the definition of “association or society”. Bodies of these types currently receive a tax exemption for certain work. |

| Aircraft maintenance reserves |

Reviewing the timing of deductibility of aircraft maintenance expenditure. |

| Remission income, insolvency and bankruptcy |

Addressing issues relating to the remission of debts in insolvency situations. |

| Lessees’ structural improvements to buildings |

Research to consider whether there is a case for allowing depreciation for lessees’ structural improvements to buildings. |

| GST technical issues |

Keeping the GST law up to date. Issues include capital-raising costs, fine metals, and the apportionment of input tax by retirement villages. An officials’ issues paper is scheduled for release in mid-2015. |

| Abusive tax position penalty |

Review the scope of the abusive tax position penalty. |

| Application of time bar to ancillary taxes |

Clarifying that the time bar on the Commissioner amending assessments to increase the amount of income tax payable also applies to ancillary taxes such as NRWT. |

| Base maintenance in line with coherent BBLR principles |

Review of whether there are sensible base maintenance measures that could be added to the work programme. |

|

Remedial work programme

|

Considering remedial matters arising from recently enacted legislation as well as other priority tax law coherence and maintenance issues, for example:

- Controlled foreign companies

- Mixed-use asset rules

- GST – on-going remedial issues

- Life insurance

- Financial arrangements

- Student Loan Scheme Act

- Working for Families tax credits

|

| Social policy |

| Child support legacy debt |

Consideration of child support debt analytics and development of further policy options to address child support debt. |

| Student loans – reciprocal agreement on cooperation between Australia and New Zealand |

Development of an information-sharing agreement between New Zealand and Australia for exchanging student loan borrower contact information to aid in the recovery of student loan debt. |

| Simplifying the tax and transfer system |

Consideration of whether the tax and transfer system can be amended either legislatively or operationally to reduce complexity for individuals as part of the first stage of Business transformation work. |

| KiwiSaver HomeStart |

To extend the current KiwiSaver withdrawal rules for first-home buyers from 1 April 2015. This is part of the “HomeStart” package announced by the Government in August 2014. |