Chapter 1 - Introduction

1.1 A key element of an efficient tax system is certainty. That means a person’s liability for tax should be as clear and as certain as possible, especially in New Zealand where the tax system is based on self-assessment. This issues paper focuses on the taxation of land disposal provisions in the Income Tax Act 2007, in particular section CB 6, which is causing some considerable uncertainty for taxpayers, their agents and Inland Revenue.

1.2 Section CB 6 deals with land acquired for the purpose of, or with the intention of disposal, and the taxation of income derived from disposing of the land. If a taxpayer acquires the land with the intention or purpose of disposal and subsequently disposes of the land, any profit made from the disposal is taxable.

1.3 The uncertainty is caused by the timing of when the taxpayer’s intention or purpose should be determined. The Courts have held that intention or purpose should be tested when a taxpayer has acquired the land in question (known as the date of acquisition). However because the definition of “land” in the Income Tax Act 2007 includes estates and interests in land, and the taxpayer acquires different interests and estates in “land” at different times under a typical sale and purchase agreement, which are then merged when the title is registered, neither the legislation nor common law have provided sufficient clarity over which interest in “land” the date of acquisition should apply to.

1.4 As a result, taxpayers may be unable to self-assess whether gains made from a disposal of land should be returned as taxable income. Often taxpayers are only made aware of a tax liability as a result of an Inland Revenue audit.

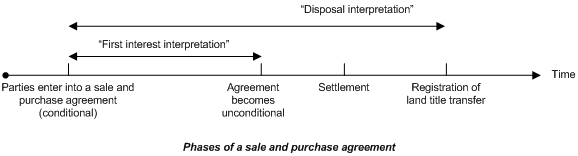

1.5 There are two possible ways of interpreting section CB 6:

- The “first interest interpretation” whereby the date of acquisition is the date when the first interest (equitable or legal) in land arises under an agreement for the sale and purchase of land (the “first interest” interpretation). Under this interpretation the date of acquisition is likely to be either the date the sale and purchase agreement is entered into or the date when the conditions of the agreement are fulfilled (that is, the purchaser is able to enforce the agreement).

- The “disposal” interpretation whereby the date of acquisition is dependent on the interest or estate that is disposed of and when the taxpayer acquired that particular interest or estate in land. This can occur at any point in the agreement.

1.6 There are potentially numerous dates of acquisition in each interpretation, as shown in the following diagram.

1.7 The two different interpretations have sometimes resulted in taxpayer uncertainty about which date to apply to their land transaction(s) and, in some cases, unintended tax outcomes. This can be a particular problem when land has been purchased off the plans and the land title has not yet been registered. This is exacerbated if agreements for the sale and purchase of land span a number of months or years or if the interest in land is assigned or disposed of to another person before the title transfer is registered.

1.8 From a tax policy perspective, the “first interest” interpretation, whereby the intention or purpose of the taxpayer is tested on the date the first interest (equitable or legal) arises in a sale and purchase agreement, is the preferred interpretation as it results in greater certainty and therefore is more economically efficient. It is the initial decision-making that informs how a person intends to use the property, and it would be unusual for a property speculator to enter into a sale and purchase agreement unless they thought it very likely that the purchase and its subsequent disposal would be profitable.

1.9 This issues paper discusses:

- the reasons for the “first interest” interpretation being preferred over the “disposal” interpretation;

- the arguments for and against the possible phases that the date of acquisition could be set at in the first interest interpretation (either when the agreement is entered into, or the agreement becomes unconditional and the purchaser can seek enforcement of the agreement); and

- whether further guidance is needed on evidential issues that may arise due to the date of acquisition falling at the earlier phases of a sale and purchase agreement.

1.10 It is acknowledged that if the Government chooses to clarify the date of acquisition, taxpayers will have the opportunity to alter their behaviour under either interpretation to avoid evidence of having an intention or purpose of resale. It may also capture some taxpayers for whom the policy is not intended. However, this risk already exists under the current legislation and if the legislation is sufficiently clarified, greater transparency should benefit all parties.

1.11 As mentioned above, this issues paper focuses on section CB 6 of the Income Tax Act 2007 however, the date of acquisition affects most of the land provisions in subpart CB. Therefore clarifying the date of acquisition in section CB 6 will be a positive step towards clarifying most of the land taxing provisions in sections CB 7, CB 9, CB 10, CB 14, CB 15, CB 18 and CB 19.

Suggested options

1.12 This paper suggests two possible options for determining a date of acquisition, based on events/phases of an agreement for the sale and purchase of land − either:

Option 1 when an agreement for the sale and purchase of land is entered into; or

Option 2 when an agreement for the sale and purchase of land becomes unconditional and the equitable remedy of specific performance of the land transfer is available to the purchaser.

1.13 We welcome views on these two options and also whether a legislative amendment is needed that allows for evidence presented before and after the date of acquisition to be considered when determining what the taxpayer’s intention was on the date of acquisition.

Application date

1.14 For ease of administration and in the interests of fairness, if the Government does decide to clarify the date of acquisition following feedback on the options presented here, we suggest that the date of application for any legislative option (that is, for new acquisitions as opposed to new disposals) be prospective from the date of Royal assent of the relevant tax bill.

Submissions

1.15 You are invited to make a submission on the proposed reforms and points raised in this issues paper. Submissions should be addressed to:

Clarifying the acquisition date of land

C/- Deputy Commissioner, Policy and Strategy

Inland Revenue

PO Box 2198

Wellington 6140

1.16 Or email [email protected] with “Clarifying the acquisition date of land” in the subject line.

1.17 Electronic submissions are encouraged. The closing date for submissions is 28 June 2013.

1.18 Submissions should include a brief summary of major points and recommendations. They should also indicate whether the authors would be happy to be contacted by officials to discuss the points raised, if required.

1.19 Submissions may be the subject of a request under the Official Information Act 1982, which may result in their release. The withholding of particular submissions on the grounds of privacy, or for any other reason, will be determined in accordance with that Act. Those making a submission who consider there is any part of it that should properly be withheld under the Act should clearly indicate this.