GST remedial matters

Overview

Most of the GST remedial items in the bill relate to issues outlined in the GST issues paper, GST remedial issues, released in December 2012. Hence, the majority of the amendments were developed from submissions received on that paper. All section references relate to the Goods and Services Act 1985 unless stated otherwise.

SCOPE OF THE “HIRE PURCHASE” DEFINITION

(Clause 123(19) and (180))

Summary of proposed amendment

The definition of “hire purchase agreement” will be broadened to include any contract where a person has an option to purchase.

Application date

The amendment will apply from 1 April 2005, with a “savings” provision for taxpayers who filed returns under the contrary position up until the date of introduction of the bill.

Key features

The definition of “hire purchase agreement” under section YA 1(a)(i) of the Income Tax Act 2007 and section OB 1(a) of the Income Tax Act 2004 will be amended to explicitly incorporate contracts under which the person has an option to purchase, but that option is not exercised until a later date.

Background

The definition of “hire purchase agreement”, in section YA 1 of the Income Tax Act 2007 is intended to cover two types of agreement. The first is when the goods are let or hired to a person with an option to purchase (an “option to purchase agreement”). The second is when a person has agreed to purchase the goods with a condition (a “conditional contract of sale”). The main difference between the two is whether the person has agreed to purchase the goods at the time the relevant contract is entered into.

An amendment made to the “hire purchase agreement” definition that took effect from 1 April 2005 contained a drafting error, which arguably means a person’s upfront agreement to purchase the goods is required in order for an arrangement to be a hire purchase agreement. This interpretation is inconsistent with the original policy intent, which is to capture both forms of agreement.

The proposed amendment was previously included in the Taxation (Annual Rates, Returns Filing, and Remedial Matters) Bill 2011. However, it was withdrawn for further consultation alongside the proposal for deferred settlement land transactions to be removed from the hire purchase definition (so as to remove the requirement for the up-front payment of GST) and be replaced with an anti-avoidance rule. These issues were further consulted on as part of GST remedial issues. After considering submissions, a decision was made to proceed with the more minor change to the hire purchase definition by extending its scope to include “option to purchase” agreements.

DWELLING DEFINITION – RETIREMENT ACCOMMODATION

(Clause 161(1) and (2))

Summary of proposed amendments

Two proposed amendments to the dwelling and commercial dwelling definitions will clarify that residential units in retirement villages and rest homes where the occupants are essentially living independently are treated as GST-exempt “dwellings”.

Application date

The amendments will apply from 1 April 2011. However, in recognition of the transitional costs to taxpayers, the amendments will be subject to a “savings” provision for those who filed their tax returns on the reverse basis up until 31 March 2015.

Key features

The proposed amendment to the “dwelling” definition will create a new subparagraph 2(b)(iii) which states that when the consideration paid or payable for the supply of accommodation in a retirement home or village is for the right to occupy a residential unit, the unit will be treated as a dwelling.

The proposed amendment to the “commercial dwelling” definition will replace section 2(b)(ii) with a cross-reference to the new amendment to the “dwelling” definition. This will ensure that units in retirement villages where the occupants are living independently are excluded from the “commercial dwelling” definition.

Background

GST is imposed on accommodation in “commercial dwellings” such as hotels but not in “dwellings” such as private residences, which are GST-exempt.

The definitions of “dwelling” and “commercial dwelling” were amended on 1 April 2011. The policy intention behind the changes was to clarify the boundary between these definitions, and to narrow the scope of what could be considered a “dwelling” on the basis of economic equivalence with owner-occupied homes.

Concerns have been raised that tenants of residential units in retirement villages may not meet the new dwelling definition requirement of having “quiet enjoyment” (under section 38 of the Residential Tenancies Act 1986) of their properties. As such, despite the previous treatment of these units as GST-exempt dwellings, they could be treated as “commercial dwellings” (subject to GST). This does not align with the policy intention, which was to maintain the pre-April 2011 GST treatment of retirement village accommodation.

OUTPUT TAX ON THE DISPOSAL OF LAND

(Clause 163)

Summary of proposed amendment

The proposed amendment clarifies that when input tax has been claimed in respect of the acquisition of land, output tax must be paid on its disposal.

Application date

The amendment will apply from the date of enactment of the bill.

Key features

The proposed amendment will extend the scope of section 5(16) so that it also applies to all subsequent supplies of land when any input tax credit has been claimed. The amendment will treat such supplies as being in the course or furtherance of a taxable activity and therefore subject to GST.

The extension of section 5(16) will not apply to situations when a registered person has already returned the output tax – for instance, if they have already performed the wash-up calculation in proposed section 21FB or they have paid output tax upon deregistration.

Background

If a registered person claims input tax when they purchase land, the correct policy outcome is for output tax to be paid on its sale. However, it is possible that a person could claim input tax on their land, but fail to pay output tax on its disposal if the disposal is outside the “course and furtherance” of their taxable activity. This situation could potentially arise when the use of the land before sale is solely non-taxable.

Although the issue also exists in relation to other assets, it predominantly occurs in regard to land.

DIRECTORS’ FEES

(Clause 164)

Summary of proposed amendments

Two amendments are proposed to section 6 that relate to the GST treatment of fees paid to directors and board members.

The first proposed amendment provides that when an employee is engaged by a third party to be a director or board member, and the employee is required to account to the employer for any payments received, the employer will be treated as supplying services to the third party. The employer will therefore return GST and the third party will be able to claim input tax on the payment for these services.

The second proposed amendment extends the proviso under section 6(3)(b) that deems services performed by directors to be supplied in the course and furtherance of a taxable activity when that director has a broader taxable activity to persons listed in section 6(3)(c)(iii) such as members of boards.

Application date

The amendments will apply from the date of enactment of the bill.

Key features

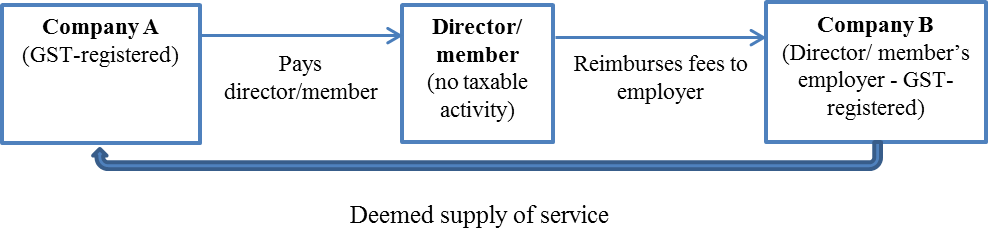

The first amendment creates a “flow-through” rule (shown below) that deems services to be supplied by an employer (Company B) to a third party (Company A) when an employee is engaged by the third party to be a director or person listed in section 6(3)(c)(iii) (that is, board members) and when the employee is required to account for any fees or other amounts to their employer (Company B). Hence, the rule will require the employer (Company B) to issue a tax invoice for the fees paid and the third party (Company A) will be able to claim the related input tax deduction.

Flow-through rule:

The second amendment extends the provision that deems services performed by directors to be supplied in the course and furtherance of a taxable activity when that director has a broader taxable activity to persons listed in section 6(3)(c)(iii) (Members of boards).

Background

The first amendment relates to an issue identified in an Inland Revenue Public Ruling (BR Pub 05/13) regarding the GST treatment of directors. It occurs when an employee who is not GST-registered is engaged by a third party to be a director and is required to remit fees paid by the third party to their employer.

In this situation, the directors’ fees paid to the employee are not subject to GST because the employee is precluded from having a taxable activity. However, when the employee passes these fees on to their employer, the employer is required to account for output tax on the supply.

This result means that the third party will not receive an input tax deduction for the fees paid. The director’s employer will, however, have to account for output tax on the amount reimbursed by the employee. Conceptually the same issue could arise in relation to the persons listed in section 6(3)(c)(iii), such as members of boards.

The second issue concerns the exception to the rule that precludes a director from carrying on a taxable activity, under section 6(3)(b). The rule applies when directors have a broader taxable activity, in which case their services as a director are deemed to be supplied in the course and furtherance of that taxable activity. However, members of boards and the other persons listed in section 6(3)(c)(iii) can also have broader taxable activities. For GST purposes the persons listed in section 6(3)(c)(iii) are conceptually the same as directors, therefore they should have the same treatment.

SURRENDERS AND ASSIGNMENTS OF INTERESTS IN LAND

(Clause 165(1) and (3))

Summary of proposed amendment

The proposed amendment to 11(8D) will clarify that assignments and surrenders of interests in land are subject to the zero-rating of land rules.

Application date

This amendment will apply from 1 April 2011.

Key features

The proposed amendment will replace “chargeable with tax at 0%” with “of land” in section 11(8D)(a) and (b) so the GST treatment of assignments and surrenders of interests in land would depend upon meeting the zero-rating of land requirements in section 11(1)(mb).

Background

Section 11(8D) is designed to clarify that assignments and surrenders of interests in land are subject to the zero-rating of land rules. The policy intent of this section is that assignments and surrenders of interests in land can be zero-rated when the requirements for the zero-rating of land rules are met.

However, the current wording of section 11(8D) arguably allows all “surrenders” or “assignments” of interest in land to be zero-rated, even when the other zero-rating land transaction requirements are not met – for instance, when the recipient of the supply is not GST-registered.

PROCUREMENT OF A LEASE

(Clause 165(2))

Summary of proposed amendment

The proposed amendment will ensure payments for the procurement of a lease are subject to the zero-rating of land rules.

Application date

The amendment will apply from the date of enactment of the bill.

Key features

A change to section 11(8D) will be made to ensure new interests in land through a procurement of a lease will be zero-rated, subject to the zero-rating of land requirements of section 11(1)(mb) being met.

Background

The concern is that the procurement of a lease when purchasing a business does not fall under the zero-rating of land rules. This is because an argument can be made that when a new interest has been created in the procurement transaction there is no transfer of an interest in land between the vendor and the purchaser. Therefore, any consideration payable in relation to this supply will not be zero-rated. This outcome does not create the correct policy outcome as lease procurements are arguably economically equivalent to lease assignments which are subject to the zero-rating of land rules.

NON-PROFIT BODIES EXEMPTION

(Clause 167(1) and (3))

Summary of proposed amendment

The proposed amendment will clarify that non-profit bodies can claim all of their GST input deductions other than on inputs that relate to the making of exempt supplies.

Application date

This amendment will apply from 1 April 2011.

Key features

The proposed amendment will ensure that non-profit bodies can claim all of their GST input deductions except those that relate to exempt supplies. It achieves this by extending the application of section 20(3K) so that it applies for the purposes of section 20(3) and (3C), and the definitions of “percentage actual use” and “percentage intended use” in section 21G(1).

Background

Non-profit bodies are able to take advantage of a special input deduction rule that allows them to claim input tax deductions on all supplies received except to the extent that the goods or services in question are used for making exempt supplies. However, an unintended consequence of the introduction of the new GST apportionment rules in April 2011 is that they have created some uncertainty around the application of the special rule.

This is because the definitions of “percentage actual use” and “percentage intended use” only enable input deductions to the extent that goods and services are actually used for making “taxable supplies”. Hence, it is arguable that non-profit bodies may not be able to claim input tax credits for purchases that relate to non-exempt supplies.

The new apportionment rules were not intended to alter the GST input entitlements of non-profit bodies.

ALLOWING INPUTS TO REGISTERED PERSONS SUBJECT TO THE DOMESTIC REVERSE CHARGE

(Clause 167(2) and (3))

Summary of proposed amendment

The proposed amendment will ensure that section 20(4B) does not prevent a person from claiming an input tax credit in cases when they are already registered for GST.

Application date

The amendment will apply from 1 April 2011.

Key features

The proposed amendment will extend the scope of the exclusion in section 20(4B) to cover a person that is already registered. This will mean that if a purchaser was already registered for GST when they incorrectly zero-rated a transaction they will still be able to claim an input tax credit.

The extended exclusion will only apply to the extent that the person uses the goods for making taxable supplies.

Background

The supply of land to registered persons is zero-rated in order to prevent “phoenix fraud”[14] arrangements. However, in limited situations this treatment can enable purchasers to avoid paying GST by intentionally or unintentionally representing that they are GST-registered and making the relevant taxable supplies. The “domestic reverse charge” mitigates this risk by requiring the purchaser in this situation to account for the output tax on the sale of the land, but preventing the purchaser from claiming an input tax deduction in relation to this sale (unless they subsequently become registered).

What is not catered for is a purchaser who is already GST-registered and incorrectly zero-rates a transaction – for example, as a result of a genuine error. Output tax will be payable under section 20 with no corresponding input tax credit.

WASH-UP RULE FOR TAXABLE OR NON-TAXABLE USE

(Clause 168)

Summary of proposed amendment

The proposed amendment will require taxpayers who have applied the apportionment rules to perform a “wash-up” calculation when their use of an asset changes to 100 percent taxable or 100 percent non-taxable use.

Application date

The amendment will apply from the date of enactment of the bill.

Key features

The proposed amendment will, for assets that have been subject to the apportionment rules, require taxpayers to perform a compulsory “wash-up” calculation to account for any unclaimed input tax or pay output tax when the use of the asset changes to solely taxable or non-taxable.

Under the proposed rule:

- Taxpayers that change from mixed-use to 100 percent taxable use of an asset will be able to claim the “full input tax deduction” (definition under section 21D(2)(a)) less the “actual deduction” (definition under section 21F(3)(c)).

- Taxpayers that change from mixed-use to 100 percent non-taxable use of an asset will be required to pay output tax equal to the “actual deduction” already claimed.

Once the wash-up calculation has been performed, taxpayers will no longer be required to make any on-going adjustments.

To qualify for the “wash-up” deduction, the taxpayer would need to sustain the 100 percent taxable or non-taxable use of their asset for the current apportionment adjustment period and the next adjustment period (up to two years).

Background

A taxpayer who purchases an asset in order to use it for taxable and non-taxable purposes must apportion their input deductions to account for the non-taxable use. However, if the taxpayer changes the use of the asset to 100 percent taxable they may still be required to perform on-going input tax adjustments. This poses a compliance cost burden on taxpayers, especially in relation to long-lived assets such as land.

If taxpayers are allowed to claim a 100 percent deduction earlier to avoid this compliance burden, the logical corollary is that a 100 percent change to non-taxable use of an asset (in respect of which a partial input tax deduction has been claimed) should give rise to an offsetting output tax payment.

TRANSITIONAL RULE FOR COMMERCIAL DWELLING ACCOMMODATION ACQUISITION COSTS BEFORE 1 OCTOBER 1986

(Clause 169(1) and (3))

Summary of proposed amendment

The proposed amendment to the transitional rule in section 21HB will ensure that input tax deductions cannot be claimed for accommodation reclassified as a commercial dwelling if it was acquired before 1 October 1986.

Application date

The amendment will apply for tax positions taken after the date of introduction of the bill.

Key features

The proposed amendment to section 21HB(1) will ensure that suppliers who are required to treat their supplies of accommodation as commercial dwellings as a result of the changes to the definitions of “commercial dwelling” and “dwelling” cannot claim input tax for accommodation acquisition costs incurred before 1 October 1986. This will be achieved by replacing the requirement for the costs to be incurred before 1 April 2011, with the requirement that they were incurred between 1 October 1986 and 1 April 2011.

Background

The transitional rule was developed for suppliers of accommodation who were required to start charging GST as a result of the changes to the “dwelling” and “commercial dwelling” definitions. The rule gave these suppliers the ability to claim input tax for the acquisition costs of their newly defined “commercial dwelling” accommodation.

However, an unintended effect of the transitional rule is that suppliers affected by the definition changes can arguably claim input tax for accommodation acquired before the introduction of GST on 1 October 1986. This is contrary to the policy rationale underlying the rule as this outcome would allow suppliers to claim input tax for property acquired when no GST was incurred.

REQUIREMENT TO BE REGISTERED

(Clause 169(2) and (4))

Summary of proposed amendment

The proposed amendment to section 21HB will allow suppliers affected by the changes to the definitions of “commercial dwelling” and “dwelling” to have the option of either including or not including a commercial dwelling as part of their broader taxable activity.

Application date

The amendment will apply from 1 April 2011.

Key features

The proposed amendment to section 21HB will give a person the option to either include or not include a commercial dwelling as part of their other supplies for consideration if the supply of accommodation in the commercial dwelling is under $60,000 in a 12-month period.

The amendment will only apply to persons:

- affected by the change to the definitions of “dwelling” and “commercial dwelling”; and

- who are required to register because the inclusion of supplies from their newly defined commercial dwelling pushes them over the $60,000 registration threshold under section 51.

Background

An unintended effect of the change in the definitions of “dwelling” and “commercial dwelling” is that a non-registered person with an activity attributable to newly defined commercial dwelling accommodation (that generates turnover below the GST registration threshold of $60,000) may now have to incorporate the commercial dwelling into their “taxable activity” which may push their turnover above the registration threshold. However, it may be the case that the person would prefer not to be forced to incorporate their newly defined commercial dwelling into their taxable activity for GST purposes, and therefore have to register for GST.

MINOR GST REMEDIAL CHANGES

| Clause | Clarification changes | Reason | Application date |

|---|---|---|---|

| Clause 162 | Definition of “life insurance contract” in section 3, Meaning of The Term Financial Services. | Update the cross-reference to Accident Insurance Act (Entitlements arising from fatal injuries). | 1 April 2002 |

| Clause 165(1) and 165(3) | Section 11(8D)(b) zero-rating of land. | Clarify that commercial leases under which no contemporaneous or advance payment has been made are subject to the exception to the zero-rating of land rules. | 1 April 2011 |

| Clause 170 | Section 46(1B) non-resident registration. | Clarify that the extended period to claim refunds only applies to GST registered non-residents. | 1 April 2014 |

| Clause 171(1) | Section 54C(3)(a) non-resident registration. | Clarify the effective date of non-resident deregistration. | 1 April 2014 |

| Clause 171(2) | Section 54C(3)(b) non-resident registration. | Clarify the scope of the 5-year embargo on non-resident registration. | 1 April 2014 |

14 Phoenix fraud arrangements involve Inland Revenue refunding GST to a purchasing company, but no corresponding payment of output tax being paid to Inland Revenue on a subsequent supply because the company is wound up before making payment.